The Role of Placement Agents in GP Fundraising - Facing tough market conditions that favor established managers, should GPs retain placement agents?

Designed by Julia Mldklff, Institutional Research Group: Analysis - Juliet Clemens - Analyst, Fund Strategies; Data - TJ Mel - Data Analyst

PitchBook is a Morningstar company providing the most comprehensive, most accurate, and hard-to-find data for professionals doing business in the private markets.

Key takeaways

• 84.8% of capital raised through Q3 2022 went toward experienced managers, leaving first-time and emerging managers in a difficult fundraising position; certain GPs, therefore, may want to consider placement agents as a fundraising resource.

• While placement agents are commonly thought of as introduction services, this is only one component of their scope of work: Placement agents assist the GP through each stage of fundraising, from document preparation, data room set-up, relationship management, setting up meetings and aiding LPs to the final close of the fund.

• Placement agents cover funds of all sizes and strategies. Broadly speaking, placement agents fall into one of three categories: large-scale, boutique, and specialized, smaller firms.

• Of the 2,760 funds that closed through Q4 2022, 344—approximately 12.5%—used a placement agent to aid in their fundraising.

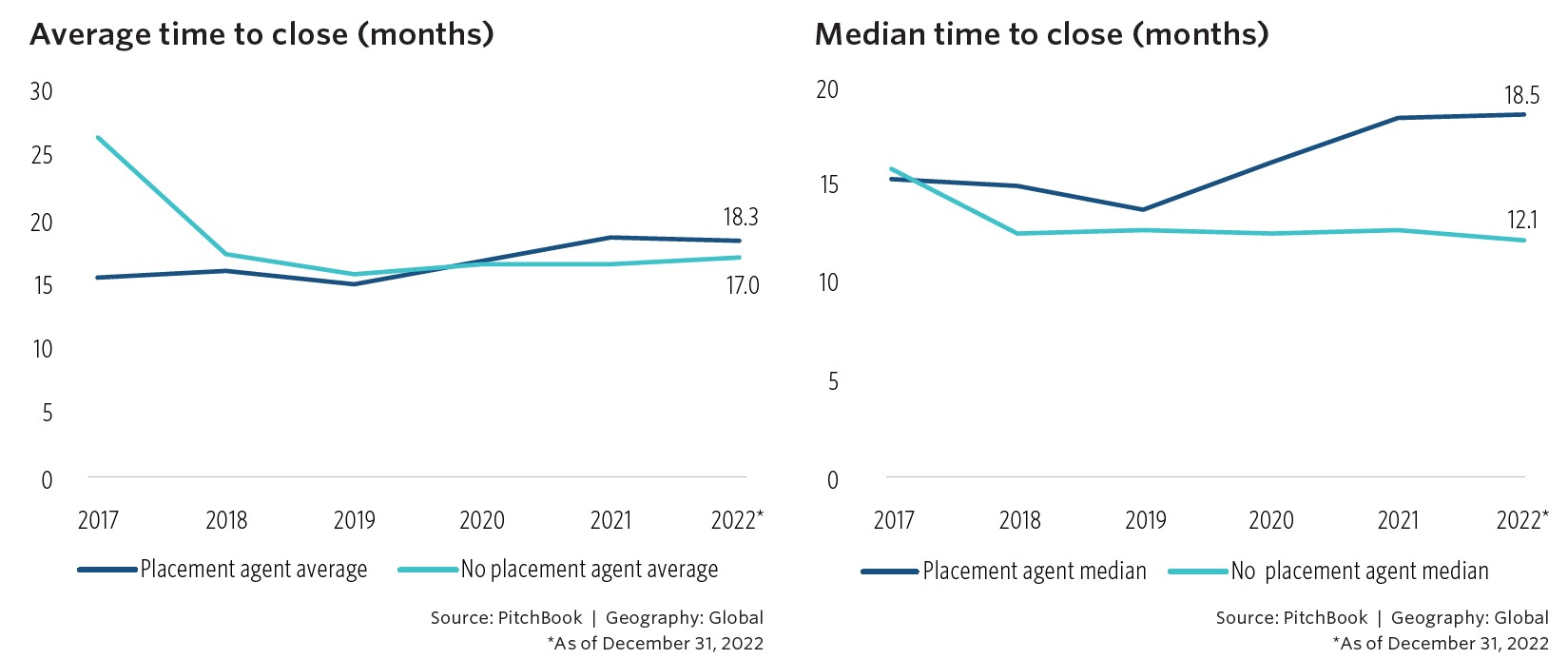

• In 2017, the average time to close for the 434 funds working with a placement agent was 15.4 months, versus the 26.4-month average of the 4,880 funds that did not work with agents. Since the pandemic, however, funds that work with placement agents spend more time on average in market than those without them: In 2021, the 698 funds retaining agents took 18.6 months to close, versus just 16.6 months for the 4,575 funds that did not.

Introduction

The fundraising environment is expected to be difficult in 2023. Private markets are still facing the numerous challenges that arose in 2022 and have persisted into the new year. Rising interest rates have struck one of the main mechanisms for generating returns—the leveraged buyout—at a time when the IPO market, a crucial exit mechanism, is still seized. The denominator effect has forced LPs to reconcile their private market-heavy portfolios, leading LPs to not only suspend making commitments to managers they have not worked with previously, but to also curb commitments to existing managers. In some cases, LPs are even selling portions of their private market portfolios on the secondary market to decrease their private market exposure or free up some liquidity, but these trades are often being done at a steep discount, given the disconnect between GP NAVs and the drop in public markets.

These unfavorable conditions make it imperative for fund managers coming to market in 2023 to be thoroughly and aggressively prepared for all aspects of the LP due diligence processes.(1) GPs are seeking capital in a market in which capital is scarce, and thus must make an incredibly cohesive, compelling case for why an LP should invest in their fund, despite extreme market volatility and risk. Most capital raised has trended toward established managers: Approximately 70.9% of capital went to experienced managers between 2011 and 2021—and the percentage has increased in recent years. Private capital fundraising totaled $926.4 billion through Q3 2022, but $785.9 billion of that figure—84.8%—went to 959 experienced managers, while the remaining $140.6 billion went to 888 emerging firms.(2) This makes the playing field incredibly difficult for emerging managers, especially those without a brand name. Given these unique challenges, it may do GPs well to consider retaining the services of a placement agent to aid them in their fundraising processes—particularly first-time or emerging managers, or managers that are looking to raise capital from a certain LP category or geography.

1: PitchBook’s Guide to Your Pitch may also be of interest to GPs planning to go to market with a fund.

2: Emerging managers are defined as firms that have raised fewer than three funds. Experienced managers are firms that have raised more than three funds.

What are placement agents?

Placement agents are hired to efficiently identify LPs who are most likely to invest with their client—the GP—and to assist the GP through the fundraising process. Agents aim to facilitate a smooth, quick fundraising process for the GPs that they represent. While placement agents are often thought of as introduction services, that is only one component of their services. Agents assist the GP through each stage of fundraising—from preparing documents, setting up the data room, managing relationships, arranging meetings, and aiding LPs to the final close of the fund.

What do placement agents do?

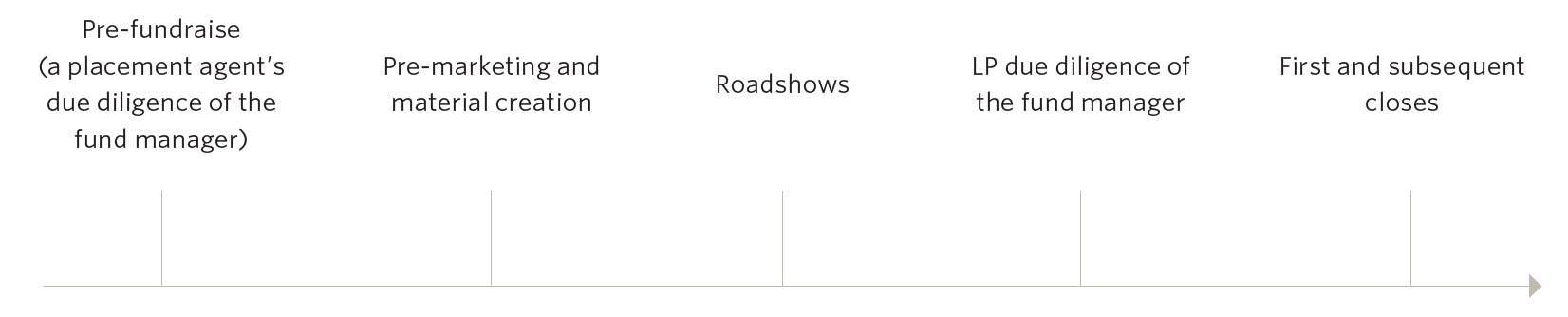

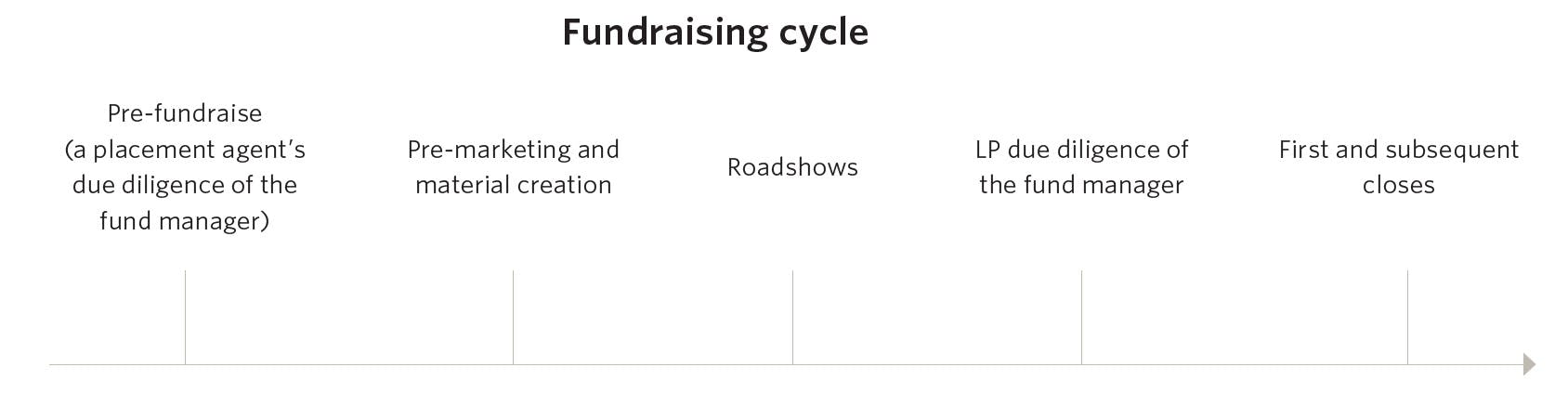

Broadly speaking, a placement agent may assist fund managers in two distinct ways: (1) by assisting their clients with marketing and due diligence materials that will prepare GPs for the extensive LP due diligence processes 3 and (2) by introducing the GP to a targeted list of potential LPs through pre-marketing meetings and roadshows, working with the GP to support an investor’s commitment into the fund. These two objectives, which will be discussed in detail further later on, are developed throughout the different stages of a GP fundraise, pictured below.

3: There are cases in which established fund managers possess the internal capacity to create their own marketing and due diligence materials and only retain a placement agent to handle the distribution to LPs for a reduced fee. Fees will be discussed in more detail below.

What different types of placement agents are out there?

Broadly speaking, placement agents fall into one of three categories: large-scale, boutique, and specialized smaller firms.

Large-scale firms can take on more mandates due to the size and expertise of their teams, although these are not hard-and-fast conditions. Larger agents will generally have a global reach and may accommodate more mandates than boutique or specialized firms—between 30 to 40 mandates per year is common—although some larger firms choose to limit their fund offerings to around 15. While larger firms are better equipped than boutique or small firms to handle target fund sizes in the multiple billions, these large-scale firms may take on clients within a wide spectrum of fund sizes. Many of the biggest placement agents accept mandates from $200 million up to $25 billion, although preferences will certainly vary. Given that established funds are more likely to have extensive in-house investor relations teams doing much of what a placement agent offers, larger agents more commonly work with smaller or mid-sized funds. The agent will typically play a niche role in carving out investors from a particular geography or LP category to help diversify the GP’s investor base.

Boutique placement agents may also have global capabilities but, because of the size of these teams, will limit their fund offerings to between five and 10 per year, allowing the agent to devote significant time and attention to each client. Because these firms are smaller, team members will often wear multiple hats, responsible for both project management as well as sales and distribution. Boutique placement agents will also typically target funds between $150 million to $5 billion, identifying potential clients within a much smaller range than a larger placement agent.

Finally, there are the smaller, specialized firms that solely target funds within a narrowly defined and niche strategy; for instance, there are placement agents that focus only on mid-cap European energy transition fund managers, or small-cap buyout managers in Southeast Asia. Many of these specialized firms are run by small teams of fewer than 10 members, and some firms do not offer the material creation component of placement agent services, opting to focus solely on the sales and distribution side instead.

A placement agent’s decision to work with a fund manager will depend on several factors, including the targeted fund size, geography, strategy, and manager’s experience level.

Why might a GP work with a placement agent?

Before exploring the ways that placement agents interact with GPs and LPs in each of the fundraising stages mentioned above, there are likely some GPs reading this note asking themselves whether to retain a placement agent. Most funds in the market do not retain placement agents: Of the 2,760 funds that closed through Q4 2022, only 344 funds—approximately 12.5%—used a placement agent to aid in their fundraising; between 2017 and 2021, just 10.3% of funds used a placement agent to close.

Fundraising without an agent is certainly possible, but it is a monumental task. A GP’s skillset lies in making deals, improving portfolio companies, and finding exits. For GPs without a strong internal IR team with the capacity to handle each stage of the capital-raising process, fundraising is often a taxing distraction from a GP’s core focuses.

Some of the benefits of working with a placement agent are:

• Help navigating marketing laws and restrictions in different geographies

• Setting up targeted introductions

• Providing informed feedback to the GP on how to relay its fund proposition

• Conveying honest and constructive criticism from LPs

Navigating marketing laws and restrictions in different geographies

Working with a placement agent ensures that the GP is working with licensed specialists who are knowledgeable about the different fundraising and marketing laws, restrictions, and requirements unique to each geography. 4 The complexity of navigating these laws varies depending on a GP’s targeted regions.

In some geographies, an offshore fund is not required to register with the country’s local financial authority given certain conditions, such as in Hong Kong, where a foreign fund does not have to register with the Securities and Futures Commission (SFC) when marketing solely to what the SFC deems “professional investors.” In other geographies, a placement agent must possess a license to market funds to qualified investors in that specific region, such as the Type II Financial Instruments Business license that allows offshore funds to market to Japanese institutional investors.

In Europe, foreign funds must work within the confines set forth in the Alternative Investment Fund Managers Directive, as well as follow the private placement rules of each country, as each country’s registration, filing, and reporting will operate very differently. Placement agents are well-acquainted with the requirements of their specialized geographic coverage and often possess a network of fund lawyers, administrators, accountants, and auditors who can advise further on such matters.

4: In some cases, it may take multiple placement agents to navigate different markets. A GP may choose to work with one placement agent to cover Asia and another to cover the Middle East, for example. There are also placement agents that cover all geographies within the same firm.

Targeted introductions

While the GP is ultimately the paying client, placement agents spend a significant amount of time speaking with LPs, even when not actively assisting on a GP fundraise. Placement agents will schedule periodic meetings with their network of LPs to hear about which products LPs are and are not interested in, how LP allocations are currently budgeted, and how much capital is available for new GP relationships. The placement agent is hearing directly from the LP about the investor’s needs, and this information can be crucial for an expedited fundraising process. Placement agents know who is not interested in a particular geography, strategy, or fund size and can provide a more targeted list to the GP, saving time by avoiding unproductive conversations.

Informed feedback

Many GPs have not had the opportunity to peruse the marketing materials of other GPs, but most placement agents have. They have also observed many LP–GP conversations and know what works and what doesn’t. Because placement agents have heard directly from a variety of LPs on several GP fundraises over the course of many years, they have effectively fine-tuned their pitches to individual GPs. For instance, first-time and emerging managers often try to fit their entire diligence package into their introductory deck, trying to answer any and all LP questions that may arise rather than focusing on the most salient points to get the LP interested in hearing more. These decks can be tedious and may not tell the GP’s story very well from the perspective of a fresh reader. An experienced placement agent knows that LPs do not want a full accounting of a GP’s history or to be pushed into signaling whether they will make a commitment to the fund at the introductory meeting. Agents know what LPs want to see from the deck, how LPs prefer decks are organized, and how GPs can make a great first impression without demanding too much too soon from an LP.

Honest and constructive criticism from LPs

The established relationships between LPs and the placement agent provide a secondary benefit: Hiring a placement agent can create a healthy mechanism by which LPs are comfortable giving the agents direct, honest feedback regarding a particular GP. The GP would likely not hear this LP feedback without the placement agent navigating between the two parties.

Why might a GP not work with a placement agent?

Working with a placement agent does not guarantee that a fundraise will be short

One reason GPs hire placement agents is to shorten the fundraising timeline. Until recently, there was evidence that a fund working with a placement agent would spend less time in market than a fund that was not working with one. In 2017, the average time to close for the 434 funds working with a placement agent was 15.4 months, versus the 26.4-month average of the 4,880 funds that did not work with agents. The gap between these averages narrowed in 2018 and 2019, and in 2020 the gap was closed in favor of funds without agents: Funds that worked with agents spent 16.8 months to close, versus 16.5 months for those without agents. In fact, since 2020, funds that work with placement agents spend more time on average in market than those without them: In 2021, the 698 funds retaining agents took 18.6 months to close, versus just 16.6 months for the 4,575 funds that did not. The 2021 median figures tell a similar story: Funds without placement agents took 12.6 months to close, while the median for funds with agents took 18.3 months. The pandemic seems to have equalized the playing field for managers, given that LPs are now more comfortable with online due diligence.

Fees

Placement agents are generally compensated by success fees—a percentage of any LP commitments garnered through the agent’s introduction—so agents are motivated to find the most competitive products and the strongest teams to represent in market. First-time funds should expect that success fee to be at least 2% of any LP commitments that come into the fund through the placement agent’s introduction. A GP lacking a track record is a big risk, so fees will typically be higher for newer managers. There are rare instances in which a newly formed GP has a fully attributable track record from a prior firm or is spinning out of an established institution and already has a somewhat developed LP network. In these cases, the success fee may be reduced. GPs should note that it is common practice for agents to charge success fees on both new and existing investors—if an LP who joined the fund through an agent decides to re-up its allocation to a GP’s next fund, this commitment will also incur a negotiated fee. In some instances, agents will also require a retainer, particularly if the agent is tasked with the marketing material creation process.

Fundraising cycle

Pre-fundraise

The success of a placement agent is dependent on the number of fundraises it can bring to a final close. As a result, agents improve their closing rate by doing their own due diligence and choosing to work with managers that they feel will be able to successfully raise a fund. Before an agent agrees to take a fund manager on as a client, it will first conduct desktop due diligence5 to determine the basics, seeking answers to questions such as:

• What fund size is the manager targeting?

• Does the GP have a track record, and if so, are both the realized and unrealized investments strong?

• How strong is the team?

• Is there a differentiated strategy?

• Are there any conflicts of interests with the agent’s current client offerings?6

• Is there interest in the market for a fund with this size and strategy?

Based on initial surface-level diligence, the agent will determine whether to pursue a project into fuller diligence or to decline based off their findings. The placement agent will also assess the competitive landscape by determining how many other funds of a particular strategy and size are currently in the market or are about to come to market. How will the fund manager in question be able to differentiate itself from its competitors? This may be performance, team, strategy, deal sourcing networks, or any number of other factors.

5: Desktop due diligence differs from the full due diligence process, which is discussed in detail later.

6: A placement agent is very unlikely to work with a GP that has a similar strategy to that of an existing client’s; it is generally written into existing client contracts that agents will not represent a similar fund, rendering this not only an ethical issue, but a contractual one. Although a fund manager may have great fundamentals, if there are too many overlaps with an existing fund offering in terms of fund size, geography, or vertical focus, there may be a conflict of interest that wouldn’t benefit any party.

Placement agents have preferences in their clientele, too: Certain placement agents choose not to work with fund managers that have solicited capital prior to seeking an agent’s services, given that it would be difficult for the placement agent to generate new interest in a fund offering if the GP has already unsuccessfully canvassed the market. There are placement agents that reserve a significant portion of their fund offerings for first-time funds, while others refuse to work with first-time funds at all. Some of these preferences will also depend on expertise the agent has honed; for instance, an agent may have earned a reputation in a particular sector or built out a unique team in a specific geography.

If the fund in question meets the agent’s specifications in the desktop due diligence phase, they will then dive into deeper, fuller diligence to assess whether the fund manager’s historical performance (if available), team, and strategy make the fund manager both competitive and differentiated against its peers in the current fundraising environment. The agent will request and subsequently analyze various documents that highlight important fund manager and fund-level details, including but not limited to:

• The gross and net performance metrics of prior funds, as well as portfolio-level performance7

• Summaries of prior investments with information regarding sourcing routes, entry and exit metrics, and the GP’s investment thesis, which in turn allow the agent to analyze a fund manager’s sourcing, value creation, and exit strategies

• Information regarding the GP’s team, both currently and historically, including deal attribution and high-level departures and/or hirings

• Audited financials of the GP’s previous funds

• The fund manager’s environmental, social, and governance (ESG) strategy and implementation

• And, when applicable, which LPs have committed to the GP’s previous funds and how much those fund commitments were.

Based on the agent’s findings during the full due diligence cycle, the agent will choose to either represent the client or ultimately pass on the opportunity. If the placement agent can identify compelling, unique angles that exemplify the GP’s strength as a competitor, it is likely the placement agent will pursue the fund manager as a client.

This level of due diligence is helpful for both the GP that is raising commitments as well as the LPs that are considering making a commitment to the GP. It is helpful for GPs because heightened diligence on the agent’s part prepares them for the difficult due diligence questions LPs are bound to ask. How does the GP respond to an LP asking why a certain portfolio company failed? What if the LP questions the amount of leverage used in an acquisition or isn’t convinced that the sector the GP is targeting will be a lucrative one? The placement agent, having conducted their own diligence, is able to pinpoint a manager’s strengths and weaknesses, coaching the GP on how to handle these questions.

This process is equally beneficial to potential target LPs that choose to conduct their own diligence once a fund manager’s virtual data room (VDR) has launched. This VDR—discussed in more detail in the following section—will contain a variety of documents regarding both fund-level and portfolio-level performance, differentiation in strategy, sourcing capabilities, team workload and deal attribution analysis, and much more. With the help of the agent, LPs can look at the fund manager with a first layer of due diligence already completed, allowing them to review and question the work that the placement agent has done rather than having to begin their own diligence processes from scratch.

Additionally, scrutinizing a fund gives the agent the opportunity to prevent early mistakes that inexperienced GPs make; prominent placement agents tell us that GPs tend to, first, come to market too early and unprepared, and second, choose a target fund size that is way beyond the GP’s capability. Placement agents encourage the GP to remain disciplined on fund-size targets, increasing the chance of fundraising success.

7: Because first-time managers do not possess a track record, these managers can try to negotiate with their former firm about attributing deals that were done at the former firm. The strategy at the current firm should be similar to that of the former. If the first-time manager is conducting deals outside of the strategy of the prior firm, this is a red flag to placement agents, and thus would be a red flag to LPs.

Material creation and pre-marketing

Once an agent decides to take on a GP mandate, a couple things happen simultaneously. First, the placement agent’s project management (PM) team will start creating the marketing materials a fund manager is expected to provide to LPs, which are usually uploaded to a VDR for potential investors to reference during their diligence processes. The PM team will draft and finalize the marketing package, which includes the executive summary, investor presentation, private placement memorandum (PPM), and due diligence questionnaire (DDQ).

In addition to the marketing package, the PM team compiles and synthesizes a fund manager’s historical performance data to produce a series of easily readable trackrecord documents that list each investment in every prior fund, highlighting important performance metrics on both a gross and net basis. The agent will also compile other useful information, including materials about the fund manager’s team, complete with organizational charts and historical deal attribution analyses; summary investment memos; and firm policies or procedures, such as their ESG or valuation policies.

While the PM team is collating this data for the VDR, the sales and distribution (S&D) team—which is responsible for both identifying high-quality GPs they would like to represent as well as maintaining LP and investor relations—will begin what is known as the pre-marketing phase. In this phase, the GP and placement agent will meet with the GP’s existing LPs to discuss the upcoming fundraise and the possibility for re-allocations, and the agent will also begin reaching out to new investors whom they believe have a higher likelihood of being interested in the fund. The pre-marketing phase gives agents with the opportunity to closely observe how the GP relays its fund proposition and provide feedback on how best to respond to a variety of questions the LP may ask. Placement agents continuously help GPs refine their investor pitch to ensure they are delivering a compelling case for investment.

The investor presentation is useful for introductory meetings between the GP and new LPs; in these meetings, the GP walks LPs through their investment thesis, sectors of expertise, track record, and case studies that reflect the successful implementation of the GP’s strategy, as well as the lessons learned from investments that are underperforming. These introductory meetings provide LPs with an overview of the GPs, their investments, their performance against their peers, their successful outcomes, and areas for improvement.

It is extremely common for LPs to request multiple meetings before progressing to a deeper phase of diligence. LPs looking to dive deeper are then given access to the whole suite of documents the agent has prepared for the VDR, including the fundlevel and portfolio-level track record analyses, PPM, DDQ, detailed information regarding the fund manager’s team, and proposed terms for the upcoming fundraise.

Roadshows

The efforts made by the S&D team in the pre-marketing phase enable the placement agent to arrange meetings with potential target investors who have expressed interest in learning more about the GP’s fundraise. The placement agent will arrange meetings with LPs, fully managing the travel and hotel bookings. The team will try to secure as many meetings as it can at each stop to maximize efficiency, bundling into one or two days as much facetime with LPs as possible. Roadshows had historically been conducted in-person, generally in the offices of the LP, before the pandemic. While most LPs still prefer to meet GPs in-person, some of this phase of marketing may occur online if both parties are willing to do so. Physical roadshows can be grueling, and travel between meetings in a city or between cities results in fewer meetings per day than can be accomplished in an online setting. However, GPs should be prepared to travel to meet prospective clients multiple times in the lifespan of a fundraise.

LP due diligence of funds

After a roadshow meeting, an interested LP will conduct preliminary due diligence by requesting access to the manager’s VDR. Before COVID-19, it was customary for LPs to conduct on-site due diligence of GPs to be able to meet more of the investment team, as well as scrutinize operational and other supporting functions, all in one visit. Placement agents are responsible for organizing these sessions, as well as ones between the LP and any available references at a GP’s portfolio companies. It is not unusual now for these meetings to be conducted via video conferencing.

LPs will review the documents uploaded on the VDR, which will often result in LPs generating more detailed questions, sometimes via an LP’s own DDQ, that they would like the GP to answer.

These questions might refer to:

• Specific portfolio companies

• The ownership structure of the GP

• How the GP incentivizes high-level team members and how carry is distributed across the firm

• What macroeconomic and market trends in the GP’s targeted geographies look like

• How the fund size was determined

• How many deals are in the GP pipeline and how GPs select the best opportunities

• Hiring plans

As part of an LP’s diligence process, investors will also usually ask to meet with each member of the GP’s management team as well as senior executives of the investment team. These meetings provide LPs with insight into the day-to-day activities of senior team members and how the management and investment teams divide responsibilities per portfolio company.

LPs usually also conduct Operational Due Diligence (ODD) in addition to investment diligence. ODD questionnaires delve deeper into the fund manager’s operational processes and might include questions regarding:

• Regulations and compliance (including internal processes regarding non-public information or insider trading, handling conflicts of interest, AML policies, etc.)

• The stage of the GPs involvement with fund administrators (who will handle capital calls, distributions, fund accounting, etc.)

• How valuations are calculated

• Technology considerations (cybersecurity/cloud services)

• Business continuity

First and subsequent closes

Ideally, LPs will indicate their interest in committing to the fund soon after their diligence processes conclude. Their internal process often includes a proposal to their investment committee. Some LPs will let the GP know they are being recommended while others wait until they have an approval in hand. Placement agents and the fund manager’s legal counsel will be involved in negotiations regarding each investor’s Limited Partnership Agreement (LPA). LPAs outline the roles and responsibilities of both the LP and GP and the actions that each will take during the fund’s lifespan. While the bulk of each LPA will be negotiated directly between a fund’s and the LP’s legal counsels, placement agents may follow the developments in negotiations between the parties, offering advice or suggestions to the GP counsel regarding specific provisions or issues that an LP flags. There are robust discussions regarding LPAs, which may include:

• Deciding between using a European or American waterfall structure

• How management fees will change as the investment period ends and as exits are realized

• Approving or rejecting GP requests for subscription lines of credit

• Clawback provisions

• Any side letter provisions that LPs may request or require, such as whether a state pension must avoid a particular geography due to state law, or whether a cancer-fighting foundation must avoid tobacco investments due to the firm’s mission statement

As these negotiations develop, placement agents are responsible for updating prospective investors on the progress of the fundraise and encouraging LPs to work toward a fund’s first close. It is important for a placement agent to generate enough fundraising momentum to have a substantial first close; a weak first close can discourage other allocators from making commitments to the fund, forcing the fund to remain in market longer and diminishing its potential to reach the target fund size.

After the first close come subsequent closes and the eventual final close. Placement agents communicate the timing of the final closing and remaining available capacity to investors. There are instances where placement agents also handle negotiations with LPs in the event of oversubscription; if the fund is extremely popular and surpasses its target fund size, it is often necessary to amend LP allocations and institute cutbacks.

Conclusion

The economic conditions of 2023 have added an additional layer of complexity to fundraising, which is itself a complex, multi-step process; managers must deliver a compelling case for investment to LPs while also actively managing their portfolio companies in an increasingly competitive environment. For managers that feel they need guidance through the full fundraising cycle, placement agents may be an important resource to consider in navigating through the 2023 fundraising market.

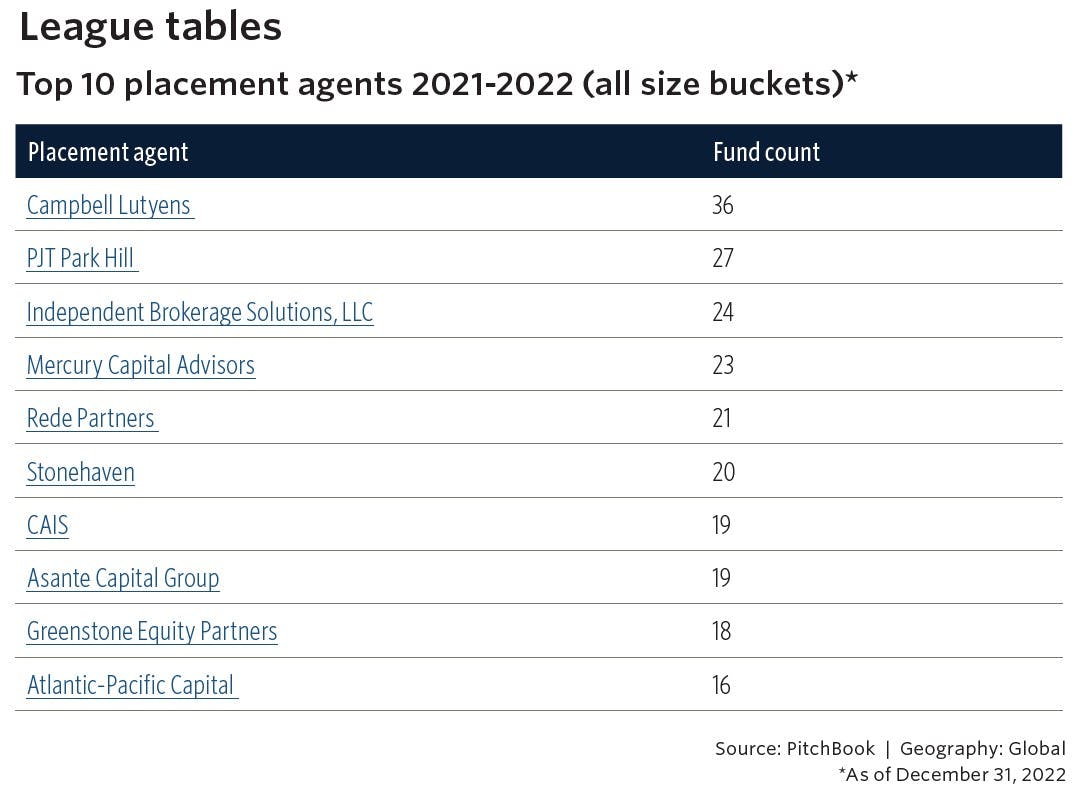

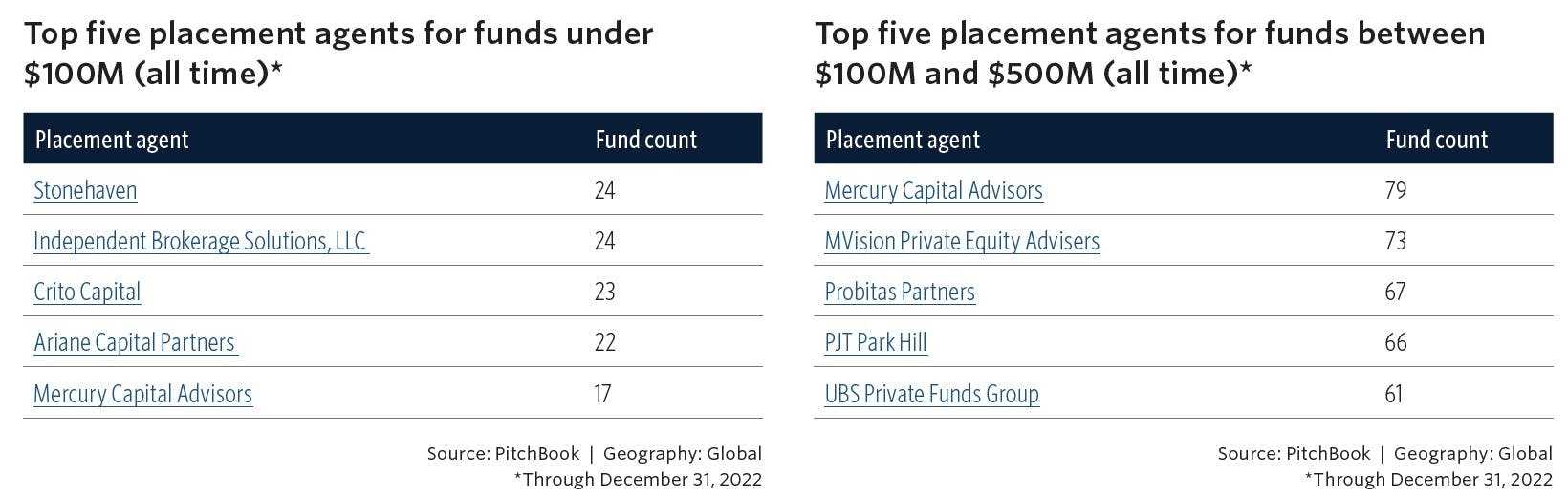

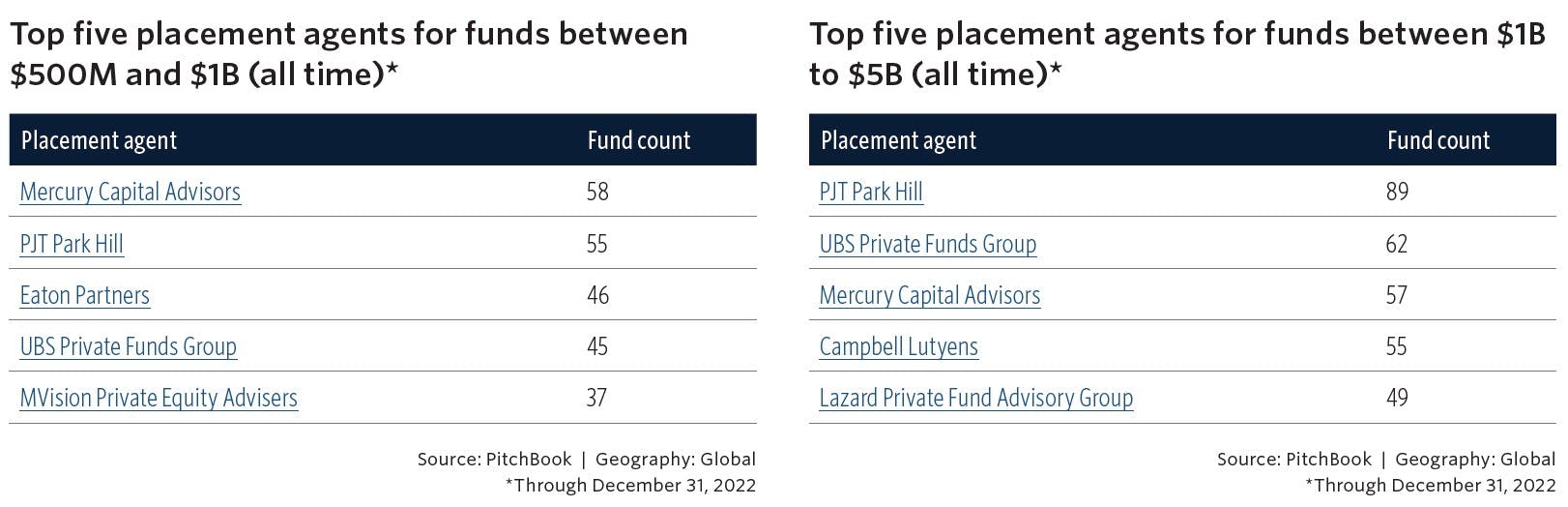

Readers will find league tables below, which split the various placement agents into specific categories based on data found on the PitchBook platform.8

8: As always, if you have any updates to data found on the PitchBook platform, you can write to survey@pitchbook.com.

See the online version here at PitchBook Data's Ranking of Placement Agents

About Stonehaven, LLC

Stonehaven is a private capital markets FinTech operating system (technology + infrastructure + data) and collaboration network (origination + distribution) for investment bankers and placement agents (Affiliate Partners) to support companies and investors. Our next generation operating system supports the entire lifecycle of deals: sourcing, contracting, due diligence, identifying target investors/buyers, managing execution (robust CRM architecture), collaborating with other dealmakers, reporting and closing transactions. Our Affiliate Partners are active across all sectors of private capital markets: raising capital, executing M&A transactions and conducting secondaries.

-

May 27, 2026

Angelica Nikolausson of ANR Capital LLC Joins Stonehaven’s Affiliate Platform

read more -

May 14, 2026

Stonehaven Chief Compliance Officer Steven Jafarzadeh Participated as a Speaker at the 2026 FINRA Annual Conference

read more